The customer data platform built exclusively for multi-unit restaurants.

.png)

Over the past several weeks, we’ve closely tracked Q3 earnings to better understand what large brands are saying about the macro environment.

So far, it’s been brutal.

McDonald's, Chipotle, and even Domino's are calling out pressure across demographics. The message is consistent: consumers are pulling back, and it's happening everywhere.

Our inaugural CMO survey from a few months ago echoed this sentiment. Of the nearly 50 marketing leaders surveyed, 66% ranked shifts in consumer spending as their top concern heading into 2026. Their commentary painted an industry that’s short on growth, struggling to articulate its value to the consumer (without over-relying on discounts), and saturated marketing channels.

That’s why the results of our inaugural CFO survey are so surprising.

Rather than mimicking the sentiment of their large brand counterparts, 80% of our respondents will have positive comp sales this year, and 67% expect traffic to grow in 2026. And despite rising costs over the last 24 months, they’ve shown enough resilience to the point where they can invest further in growth in 2026 without sacrificing margins.

Overall, the report reveals the many ways in which emerging, high-performing brands think about growth, traffic, margins, and the success of their digital efforts heading into 2026. But more importantly, it reveals an interesting, underdiscussed dynamic happening in the industry today.

Domino’s, Chipotle, McDonald’s, and others have all warned about softness in restaurant visits across demographics. Our own data recently backed this up, with some brands seeing an alarming (40%+ drop) in frequency. Overall traffic and sales might be fine, but repeat visits are harder to come by. This suggests that consumers are getting more selective with their restaurant occasions, eating out less than in prior years.

And when repeat visits dry up, trial becomes everything.

If guests aren't coming back as often, a brand’s survival instead depends on continuously winning first-time visits. This is where the results of our CFO survey get interesting - they point to a moment where smaller brands are best positioned to capture share from larger, legacy players.

A different kind of operator

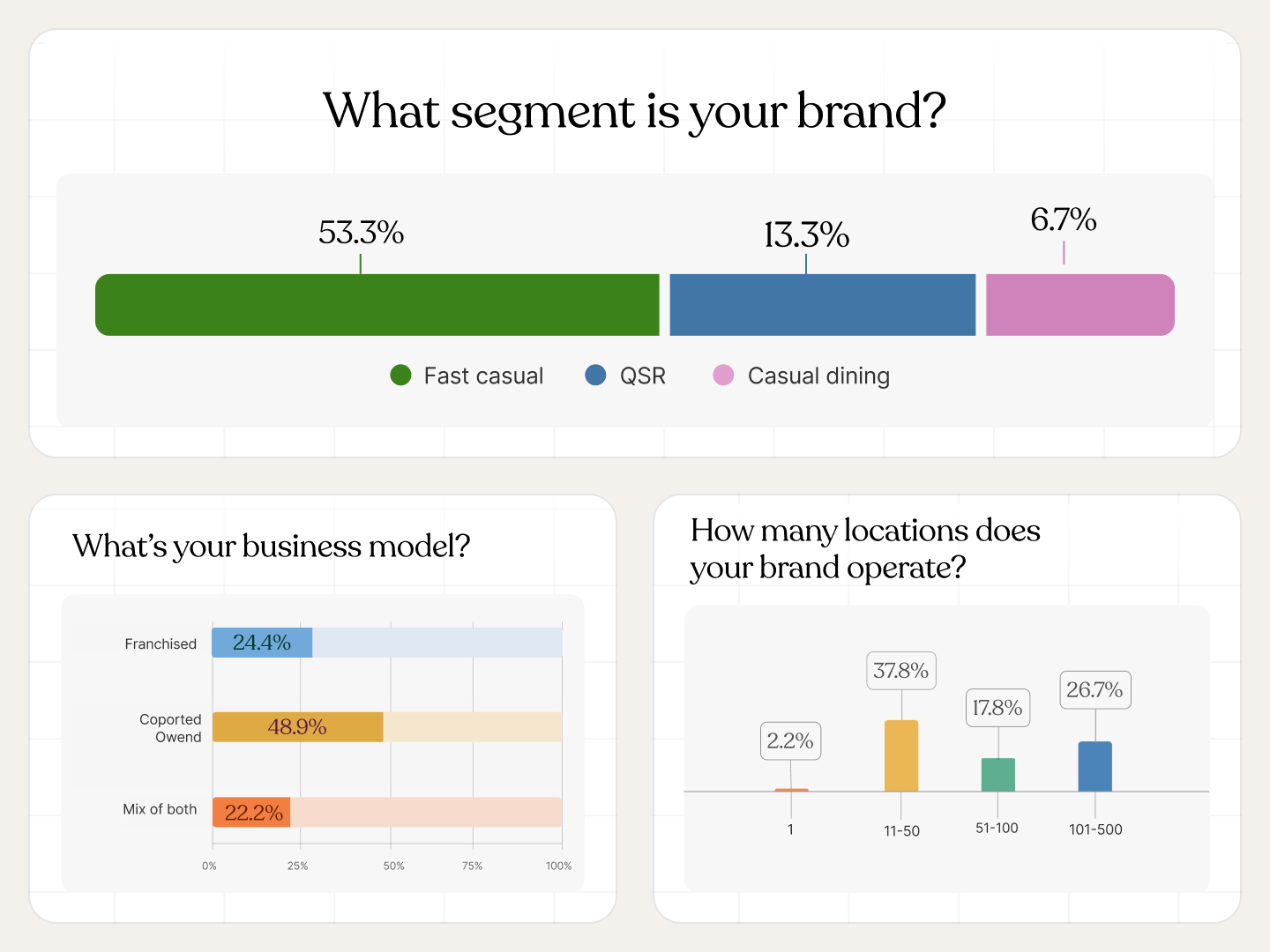

The CFOs we surveyed represent a very different restaurant landscape than the public companies dominating earnings calls. Our respondents skew toward smaller, emerging growth concepts—all operating under 500 units, with over 70% under 100 units.

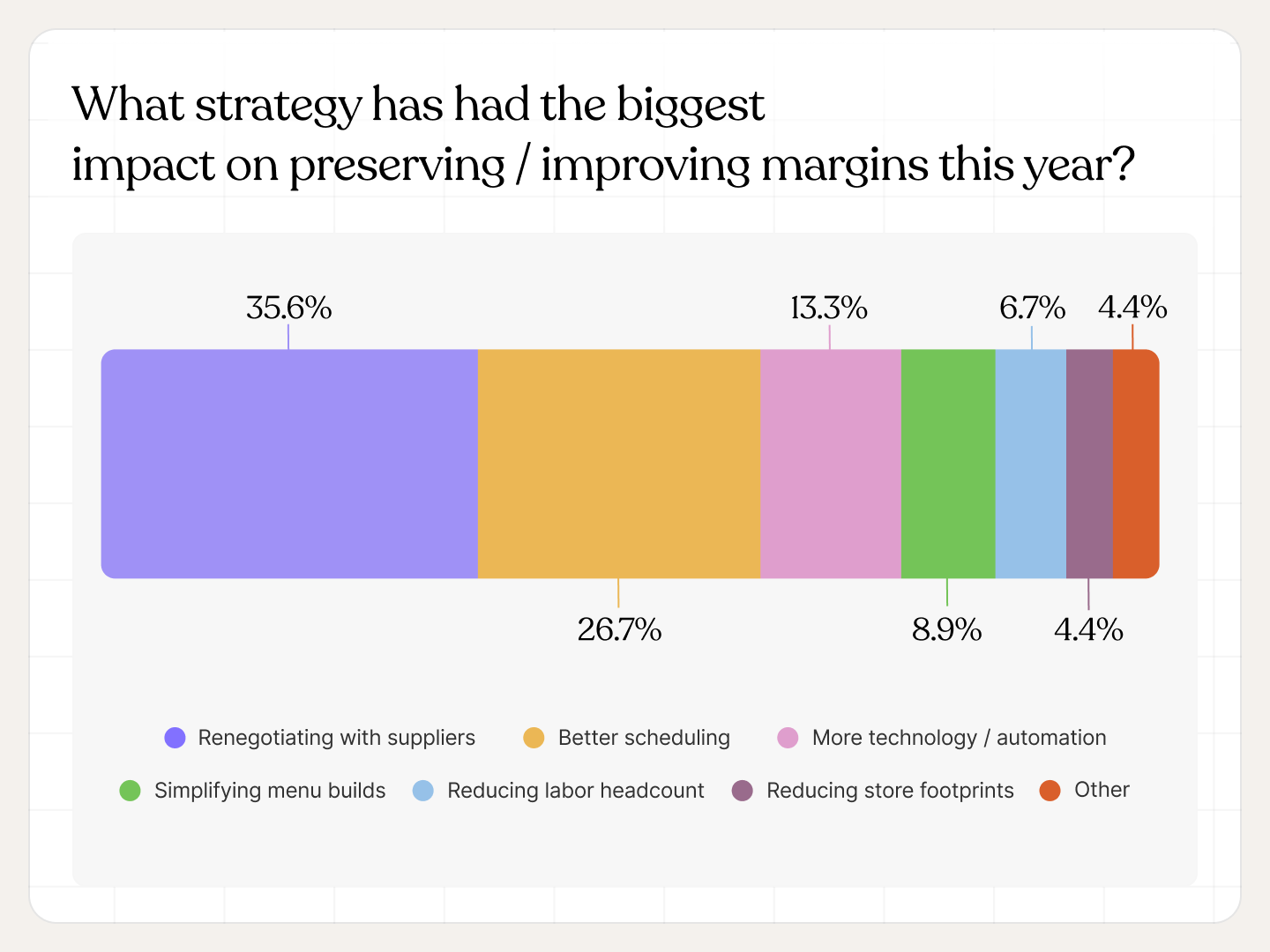

These operators are maintaining operational excellence despite rising costs. Nearly every CFO surveyed expects margins to be the same or better in 2026, even as 29% anticipate further prime cost increases (most are already at 55-60%). They're achieving this through supplier negotiations, better scheduling, and focus on controllable expenses further down the P&L, giving them room to invest in growth. 73% plan to open new stores in new markets or fill in existing ones next year, with 40% expecting strong (over 30%) cash on cash returns for new builds.

This is the core playbook for winning trial. Leverage operational efficiency to build your brand and invest in proven customer acquisition channels, like local store marketing or third-party delivery (where unit economics allow). These smaller brands also have significant headroom for growth. With smaller footprints and lower brand penetration, they're still in the phase where most guests entering their funnel are first-timers. Combined with compelling value propositions and operational excellence, this creates a real opportunity to scale through trial acquisition.

%20Where%20do%20you%20expect%20store-level%20margins%20to%20be%20next%20year_.png)

The optimism is real

To echo the key takeaway once again from the survey - the majority of brands surveyed will end 2025 with positive same-store sales, and 67% of operators surveyed expects positive traffic in 2026.

This runs counter to the oft-cited industry saying that in tough times, consumers stick with what they know—the familiar, safe, established brands. But that assumes the established brands are still delivering value. Increasingly, their own commentary shows the opposite - that their prices have risen too quickly, that consumers are craving new experiences and occasions, and that their relevance with younger and price-sensitive guests is eroding.

Smaller concepts are winning on value positioning, operational excellence, and authenticity. They're nimble enough to adapt. They're local or regional enough to feel community-focused. And they're new enough to generate curiosity and trial.

The data from our survey suggests this is already happening. The question is how long the window stays open, and which emerging brands will be aggressive enough to seize it.

%20What%20do%20you%20think%20will%20be%20the%20biggest%20driver%20of%20growth%20in%202026_%20(2).png)

In the wake of the pandemic, brands invested aggressively in building their digital ecosystems. They needed a way to maintain a connection with guests outside their four walls, and build digital experiences on par with their retail counterparts. So brands launched online ordering, loyalty programs, and third-party delivery in an effort to meet consumers where they are.

Now, a few years on from the start of those investments, we're starting to see greater skepticism around the true incrementality and ROI of these decisions - even among the high-performing operators in our survey.

The loyalty ROI question

We’ve seen a spike in loyalty-related ROI questions recently at Bikky: “How do I know a loyalty guest isn't just someone who would have come anyway? Am I just giving discounts to my most frequent guests? How do I know I'm actually driving more visits?" We’re seeing these crop up in our survey results as well, with only half of CFOs seeing positive returns from their program. Another 16% don't know (or can’t measure) if their loyalty program actually drives incremental traffic and frequency.

This presents a fascinating tension, as the CMOs we surveyed ranked loyalty and first-party as both the highest ROI tactic and fastest growing channel in 2025.

This suggests that the growth is there - and that promotions work - but the core underlying question on “true” frequency of loyalty has yet to be resolved.

%20How%20would%20you%20characterize%20the%20ROI%20of%20your%20loyalty%20program_.png)

Third-party delivery: profitable, but not incremental

On third-party delivery, CFOs are less split.

When we asked about third-party incrementality, only 31% of CFOs said the channel is at least 50% incremental. In other words, the vast majority of operators believe it's actively cannibalizing other channels. One operator we recently talked to put it plainly: "We know the convenience consumer has shifted from the drive-thru to third-party apps. Same guest, worse economics."

This dovetails with what we’ve heard from CMOs, who acknowledge growth on the channel has slowed (perhaps because it’s a larger part of the business now), and that they’ve seen a decline in the ROI on paid ads.

Despite the perceived lack of incrementality and lower margins, CFOs have done an excellent job of preserving overall profitability. 76% say third-party delivery is profitable—even when factoring in the incremental commission for ads and promotions.

%20Are%20your%20third-party%20delivery%20orders%20profitable_.png)

The tension

The two levers CMOs have most relied on to drive growth in recent years are now facing increased skepticism from their finance counterparts. CMOs need third-party platforms to drive trial and acquire marketplace consumers who may not have found their brand otherwise, and they also need loyalty programs to incentivize frequency and build a base of repeat guests they can market to directly.

But CFOs are looking at the same data and questioning whether either channel is delivering enough incremental value.

We believe resolving this disconnect will be critical in 2026. The brands that succeed next year will build programs that win at the top of the funnel, land with a compelling value proposition, and understand (through guest data) the specific aspects of their menu, operations, and marketing that lead to second and third visits.

%20What%20is%20your%20expected%20same-store%20sales%20performance%20in%202025_.png)

%20What%20are%20your%20current%20prime%20costs%20%20as%20a%20percentage%20of%20sales_.png)

%20Where%20do%20you%20think%20prime%20costs%20as%20a%20percentage%20of%20sales%20will%20be%20next%20year_.png)

%20Where%20have%20you%20seen%20the%20biggest%20increase%20in%20costs%20in%202025_.png)

%20What%20is%20your%20current%20four-wall%20EBITDA__.png)

%20What%20is%20the%20main%20focus%20of%20your%20store-level%20investment%20strategy_.png)

%20What%20are%20your%20current%20cash%20on%20cash%20returns%20for%20new%20store%20builds_.png)

%20Where%20do%20you%20think%20cash%20on%20cash%20returns%20will%20be%20next%20year_.png)

%20What%20percentage%20of%20total%20sales%20now%20comes%20from%20digital%20channels.png)

%20How%20incremental%20are%20digital%20sales_.png)

%20What%20do%20you%20think%20will%20be%20the%20biggest%20driver%20of%20growth%20in%202026_.png)

%20How%20are%20you%20planning%20to%20fund%20new%20tech%20initiatives%20in%202026_%20Greatest%20-%20Leastes.png)

%20What%20are%20your%20expectations%20for%20consumer%20sentiment%20over%20the%20next%206%20months_.png)

The customer data platform built exclusively for multi-unit restaurants.