The customer data platform built exclusively for multi-unit restaurants.

.png)

In our Q3 2025 CMO Survey, marketers clearly outlined the challenges they're facing: it’s tough to grow traffic, they’re worried about consumer spending, and third-party delivery is getting saturated. But loyalty stood out as the fastest growing channel, despite sensitivity around over-discounting.

This should come as good news - brands have invested millions in the past few years in building direct, first-party ecosystems for their guests. There are early signs that loyalty programs are generating sales, but a lack of clarity on their overall ROI. Would these guests have come anyway with a discount?

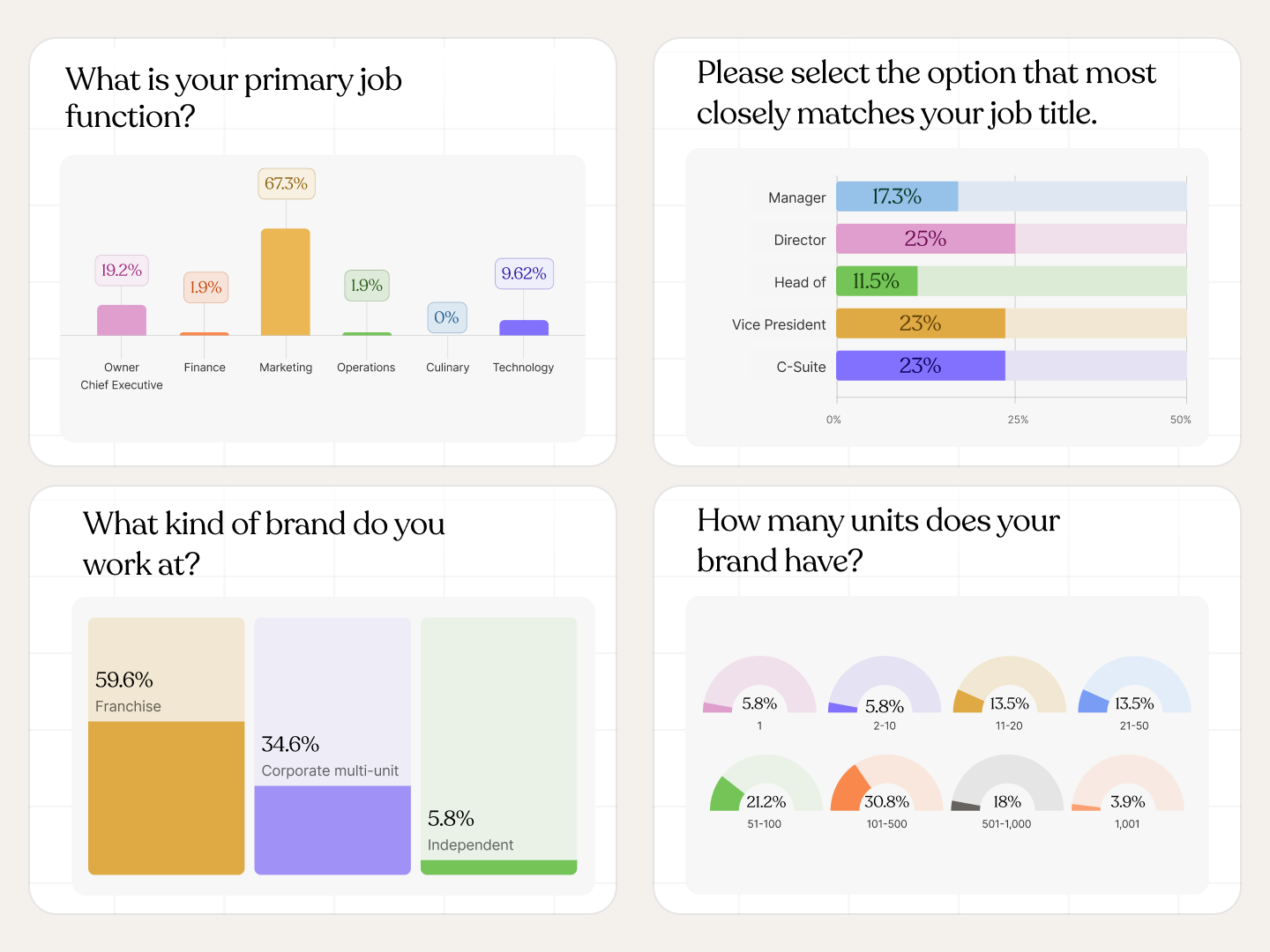

We heard from over 50 multi-unit restaurant operators and marketing leaders to tell us where things actually stand.

We decided to be bold in our first key question in the survey - how would you rate your overall satisfaction with your loyalty provider? We know restaurants believe in the value of their programs, but how do they feel about their tech partners? Overall, satisfaction is mixed, with an average score of 3.3 out of 5.

%20How%20satisfied%20are%20you%20with%20your%20loyalty%20provider%20on%20a%20scale%20of%201-5_.png)

86% of respondents flagged at least one meaningful strategic limitation with their program. While questions around ROI came in at the top, we were surprised by how evenly folks cited issues in structure, segmentation, and signups - three of the core elements of the program. On the flip side, despite the sensitivity around discounting in our CMO survey, only 22% cited guests being over-discounting as a top concern.

.%20Top%20complaints%20(multi-select).png)

Despite the mixed reviews and complaints on core structural issues in their programs, 70% of respondents expect to stay with their current loyalty provider in the next 12 months.

At a high level, operators know their programs drive frequency. 75% of respondents say loyalty members visit more often than non-members - but again, more than 40% admit they can’t measure ROI, and 17% outright say they don’t track the differences in frequency.

But the deeper questions remain largely unanswered. Would these guests have come anyway? Are loyalty members simply the brand's best guests by nature, and the program is now just layering discounts on top of behavior that would have happened regardless? And if so, does that mean operators are reducing the profitability of their most valuable customers without driving any incremental behavior?

%20How%20would%20you%20characterize%20the%20ROI%20of%20your%20loyalty%20program%20today_.png)

These important questions are the difference between a program that's working and a program that just looks like it's working, and most operators in this survey seem to be running on gut feel rather than answers.

This is a question we’ve studied rigorously at Bikky - and one of the most common ones that clients ask when they have a full view of loyalty and non-loyalty guests with a CDP. While intuitively, it’s obvious that frequency for loyalty members is higher than non-loyalty members, many marketers struggle to prove the incrementality or overall impact on lifetime value.

In both cases, the data supports the positive ROI narrative. In our work with Salad House, their team found that a guest who only ordered through loyalty was worth 7x more than a guest who never used the program - a $214 per guest difference. And in our work with MOOYAH, loyalty welcome offers for existing guests (those who visited the brand before they opted into loyalty) had a 56% repeat order rate, significantly higher than the standalone retention rate.

Most operators know their program looks like everyone else's. 82% are running a standard points-based program, only 16% have any tiered or status-based mechanic, and 39% cite their program structure as being too basic to differentiate — the second-most common complaint in the survey.

%20How%20personalized%20are%20your%20loyalty%20offers%20today_.png)

The personalization picture follows the same pattern. Over a third flagged lack of segmentation capability as a top complaint — yet nearly 30% do no segmentation at all, and another 42% rely only on basic single-variable segmentation. For most brands, their program is essentially on autopilot. The only real differentiators are the earn-and-burn structure and whatever rewards they've made available. When offers are generic, points are doing all the heavy lifting.

And yet, demand for personalization is real. Industry experts are calling 2026 the era of the "Me-Me-Me Economy," with hyper-personalization and AI-driven offers positioned as the defining loyalty trend of the year. Deloitte's 2025 Consumer Loyalty Survey found that more than half of Gen Z and millennial consumers say they would spend more with a brand that offered a personalized experience. The discourse is loud. But our survey tells a different story on the operator side — hyper-personalization is everywhere as a concept. As a practice, it remains the exception.

We see this first-hand in our work at Bikky. When brands combine like City Barbeque and Protein Bar & Kitchen use two or more variables in segmentation - like frequency and menu data - their marketing conversion rates skyrocket by 3-7x.

42% of respondents say getting more guests into the program is their top priority for 2026. This makes sense when you break down the state of most programs in our survey - over 60% of brands acquire less than 5,000 guests per month, and over 80% can attribute less than 30% of transactions to their program. It's also the most intuitive loyalty lever - the one easiest to report on, and the one that shows up most visibly in the metrics leadership tends to watch.

But it’s also the wrong primary focus for many of the brands in this survey. When you map 2026 priorities against active member rates, a few interesting patterns emerge.

.png)

The brands most in need of activation work are the least likely to prioritize it. Brands with under 20% of members active focus on acquisition the most out of everyone we surveyed, with 54% citing it as their top priority. But these are programs where four out of five members don’t transact for at least a year - the exact programs where greater emphasis should be placed further down the funnel, either on increasing the active member rate, or driving higher frequency with the guests they do acquire.

The blind spot is at 30-40% active — and it's the most common place to be. 27% of respondents fall into this bucket, making it the single largest active rate cohort in the entire survey.

These are programs that look functional, with reasonable active rates. And yet, despite continuing to grow their programs, this group does not prioritize increasing activation at all, despite the massive opportunity to do so. They've crossed the threshold where the engagement problem is visible enough to act on, but the instinct to grow top of funnel wins anyway.

The shift happens at 40%. Above 40% active, the picture changes sharply. Acquisition is much less of a priority, with 29% citing it as the primary goal at 40-50% active, and 17% above 50%. Instead, frequency becomes the dominant priority. In our opinion, this is exactly what healthy brands should be focused on. These brands have figured out how to drive at least one visit per year from their base, and instead are focused on driving that number higher. On the flip side, given the strength of their activation efforts, unlocking better top of funnel could be a massive unlock for digital / loyalty transaction growth.

The acquisition instinct isn't wrong for every brand. Programs under 50,000 members are still building a base worth activating, and acquisition is the right focus at that stage. But 67% of respondents in this survey have over 100,000 members. For most of them, the constraint isn't the size of the enrolled base. It's what happens after enrollment — and the data suggests most haven't made that shift yet.

One of the more notable findings in the survey is the gap between how marketers measure loyalty success and what the rest of the organization is watching.

Marketers gravitate toward program health metrics — 37% cited loyalty transactions as a share of total transactions as their top KPI, and 31% cited visit frequency of members versus non-members. Both measure whether the program is working mechanically: is loyalty capturing more of the business? Are members visiting more often?

%20What%20KPI%20is%20most%20important%20to%20you%20for%20measuring%20loyalty%20success_%20copy.png)

Internal stakeholders, according to respondents, care more about business-wide metrics — 35% prioritize year-over-year transaction growth, and 13% total member counts. They want to know whether the overall business is growing, not whether the program's internal health indicators are trending in the right direction.

%20What%20KPI%20is%20most%20important%20to%20you%20for%20measuring%20loyalty%20success_.png)

Neither is wrong. But they answer fundamentally different questions, and that gap could speak to an underlying communication problem. A loyalty team can show strong frequency lift and a growing active member base — and still struggle to justify the program budget to leadership who sees flat transaction growth and wonders what they're getting for it.

Brands know they’re constrained - in terms of segmentation, sign up friction, or points structure. But if they can get a handle on their funnel metrics, anchor their tactics around the gaps in that funnel, and align internally on ROI, the data reveals there’s tremendous opportunity for the year ahead. Here are the key priorities we see for 2026:

Know where you are on the maturity curve. Your 2026 priorities should follow from the size, health, and performance of your program. Most brands default to acquisition - it’s the easiest lever to pull and the easiest to report on. But the data reveals that many would benefit from increasing activation rates, with 40% being seen as a best in class benchmark (or at least when brands shift their thinking to frequency, instead of outright acquisition).

Close the gap between perceived and measured ROI. Most operators believe their program is working. Fewer can prove it — and fewer still can prove it in terms that resonate with the rest of the business. Connecting program health metrics to actual business outcomes isn't just a measurement exercise; it's what makes loyalty defensible at budget time and credible to the stakeholders who matter.

Use your data, not just your platform. The brands seeing the clearest results from loyalty aren't necessarily on better platforms — they're doing more with what they already have. Behavioral segmentation, incrementality measurement, and offer personalization don't require a new provider. They require actually using the guest data you're already sitting on.

The customer data platform built exclusively for multi-unit restaurants.